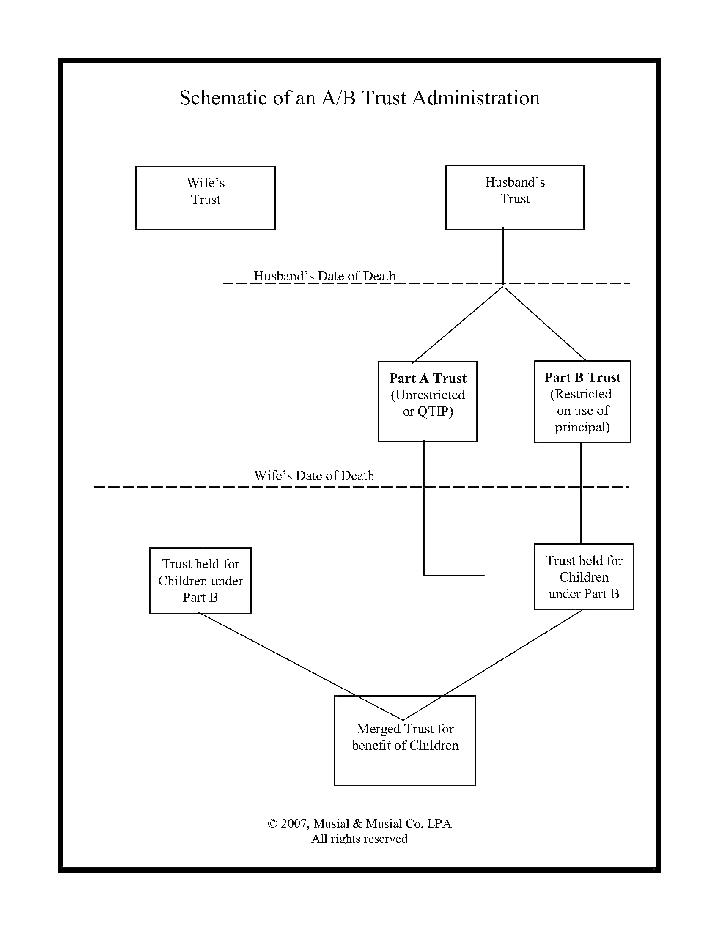

For a married couple with a large estate (meaning in excess of twice the value of the Federal exemption equivalent, which is currently $11,700,000, including the face value of your life insurance for 2021), an Estate Tax Savings Trust, in addition to providing all the benefits of a Revocable (Living) Trust, can also generate substantial savings of Federal estate taxes. An Estate Tax Savings Trust is also sometimes called an "A/B trust" or a "credit shelter trust".

With an Estate Tax Savings Trust, a portion of the funds are allocated to a sub-trust (the Part B) for the children upon your death. This portion can pass federal estate tax free through the use of federal estate tax credits. The remaining assets may be allocated to a separate trust solely for the spouse, or given to the spouse directly. There will be no federal estate tax upon death of the first spouse, and when the surviving spouse subsequently dies, the assets in the children's trust are nontaxable assets for both Federal and Ohio estate tax purposes.

The surviving spouse can have full management control over the property allocated for him or her in the trust, and also can receive the income from the children's trust. Further, a portion of principal from the children's trust can be made available to the surviving spouse each year. The surviving spouse can even be the trustee of both trusts, and therefore continue to manage all of the assets.

The savings in estate taxes with this type of trust can be substantial. For example, on a larger estates the Federal estate tax savings alone can be on the order of 35% of every dollar above the Federal estate tax exemption equivalent in 2012, and as much as 40% in 2013 and 2014 under the current rules. The end result is that the surviving spouse and children can be well cared for while maximizing the funds available to the children by reducing estate taxes.

Congress has made some changes to the Federal Estate Tax law effective January 1, 2013. The exemption amount (for Federal Estate Taxes) for for those who passed away in 2020 is $11,580,000 ($11,400,000 if death was in 2019). The tax laws were also changed to permit the portability of that exemption to a surviving spouse. This means that a surviving spouse can claim the unused portion of their spouse's exemption, and have it available when the survivor passes away. Thus, a couple can leave as much as $22,800,000 to their beneficiaries before any Federal estate tax would be due. In order to claim the porting of the exemption, however, the surviving spouse must timely file an estate tax return in their decesed spouse's estate. Otherwise the porting is lost.

We have also had some significant changes in the Ohio Estate tax rules. For 2012, the Ohio Estate Tax exemption equivalent remained at $338,333, with an estate tax rate of 6% for those estates between $338,333 and $500,000, and a rate of 7% for the portion above $500,000. Commencing in 2013, the Ohio estate tax has been repealed. That means there are no estate taxes to pay for Ohio estates, regardless of its size for estates of individuals who pass away after January 1, 2013.

So, with these high exemptions, is there still a need for an estate tax avoidance type of trust. The answer, as it always seems to be, is that it will depend. If a trust is used to trap the estate tax exemption in the first spouse's estate, those assets, and what ever they grow to will continue to escape estate taxation. Additionally, there will be the other benefits with having the assets held in the trust; such as future creditor protection, or controlling future distributions. A planning evaluation will have to be made as to whether you expect the assets to increase in value more than the rate of inflation for future increases in the estate tax exemption amounts.